Most backtests lie. Validation is how you catch them.

With enough tuning, almost any strategy looks brilliant on history. The only thing that separates real edge from curve-fit noise is how it performs on data it was never fitted to — and that takes more than one backtest.

The curve-fitting trap

Give an optimizer enough freedom and it will find a set of rules that nailed the last few years perfectly. The equity curve slopes up and to the right, the profit factor is gorgeous, and none of it means anything — because the strategy memorised noise that will never repeat.

The fix isn’t a better backtest. It’s testing the same strategy several different ways, each designed to expose a different kind of overfitting, and only trusting what survives all of them. That’s what Verdict Strategy Builder does to every candidate, automatically.

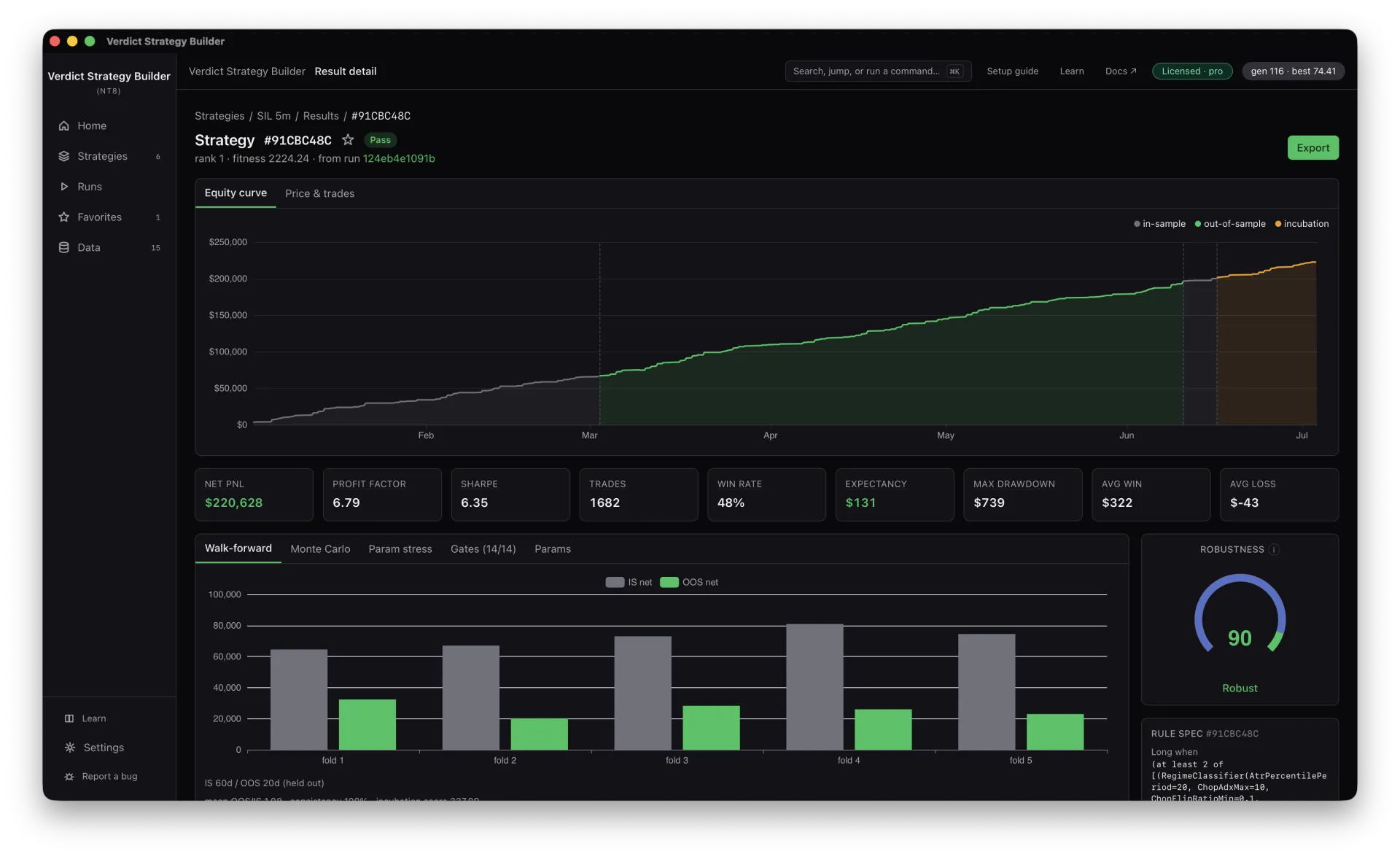

Walk-forward & out-of-sample

The engine optimizes on one window and measures on the next, rolling forward through history. A strategy only looks good if it keeps working on data it was never fitted to — the single most honest test of whether an edge is real.

- Optimize in-sample, measure out-of-sample, roll forward

- A held-out incubation window the search never touches

- Consistency across folds, not one lucky period

Monte Carlo resampling

One equity curve is a single ordering of trades — and ordering flatters luck. Monte Carlo reshuffles and resamples thousands of times to reveal the distribution of outcomes: the drawdown you should actually plan for, not the one you happened to get.

- Percentile equity bands from thousands of resamples

- Worst-case drawdown at p95 and p99, not just the average

- Confidence that survives reordering, not just one path

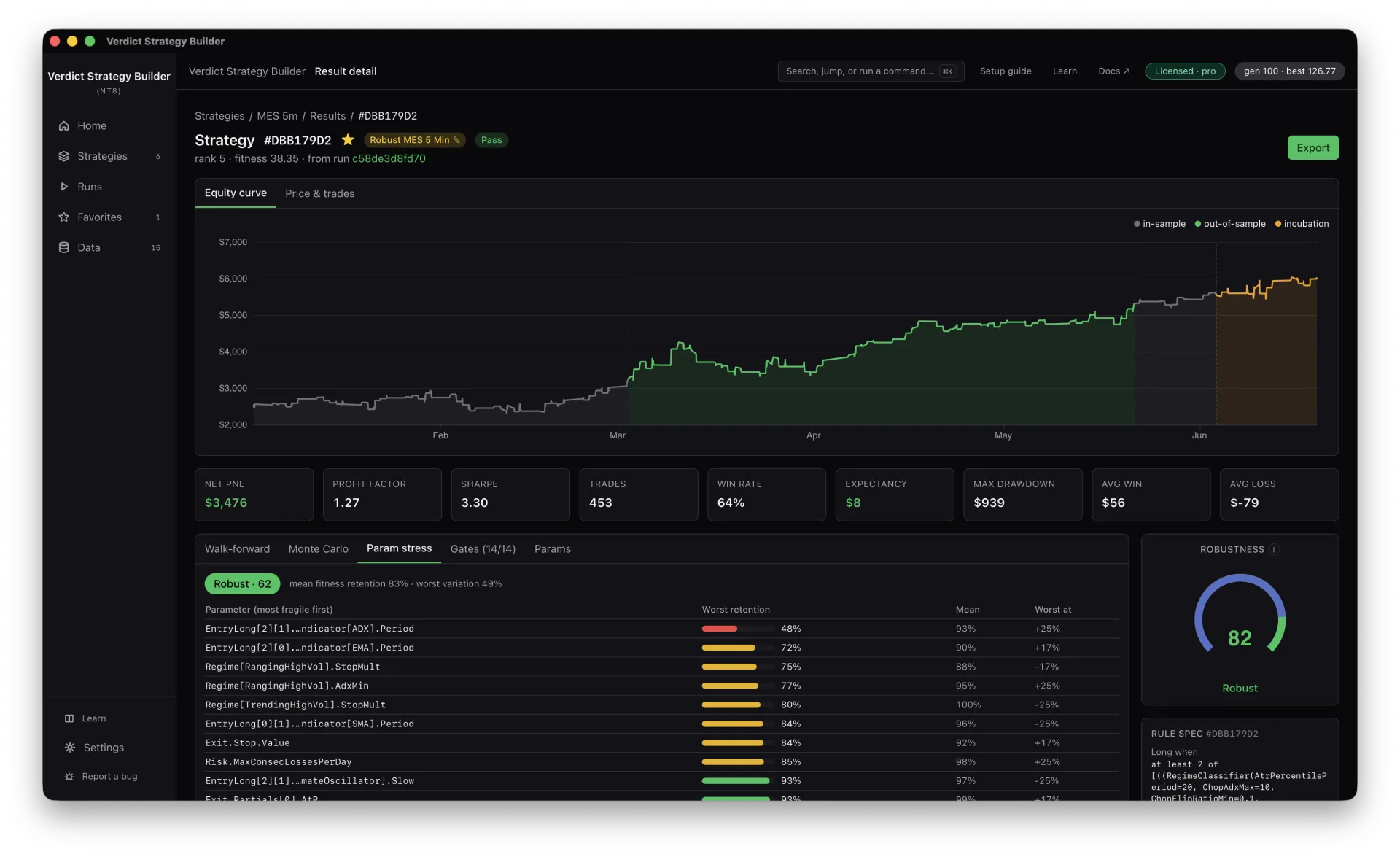

Parameter stress

A robust edge does not hinge on one magic number. Parameter stress nudges every setting through its neighborhood and measures how much fitness survives. Cliffs mean curve-fit; plateaus mean something real.

- Every parameter perturbed through its local range

- Fitness-retention scored, most fragile surfaced first

- Fragile, knife-edge fits are caught before you trade them

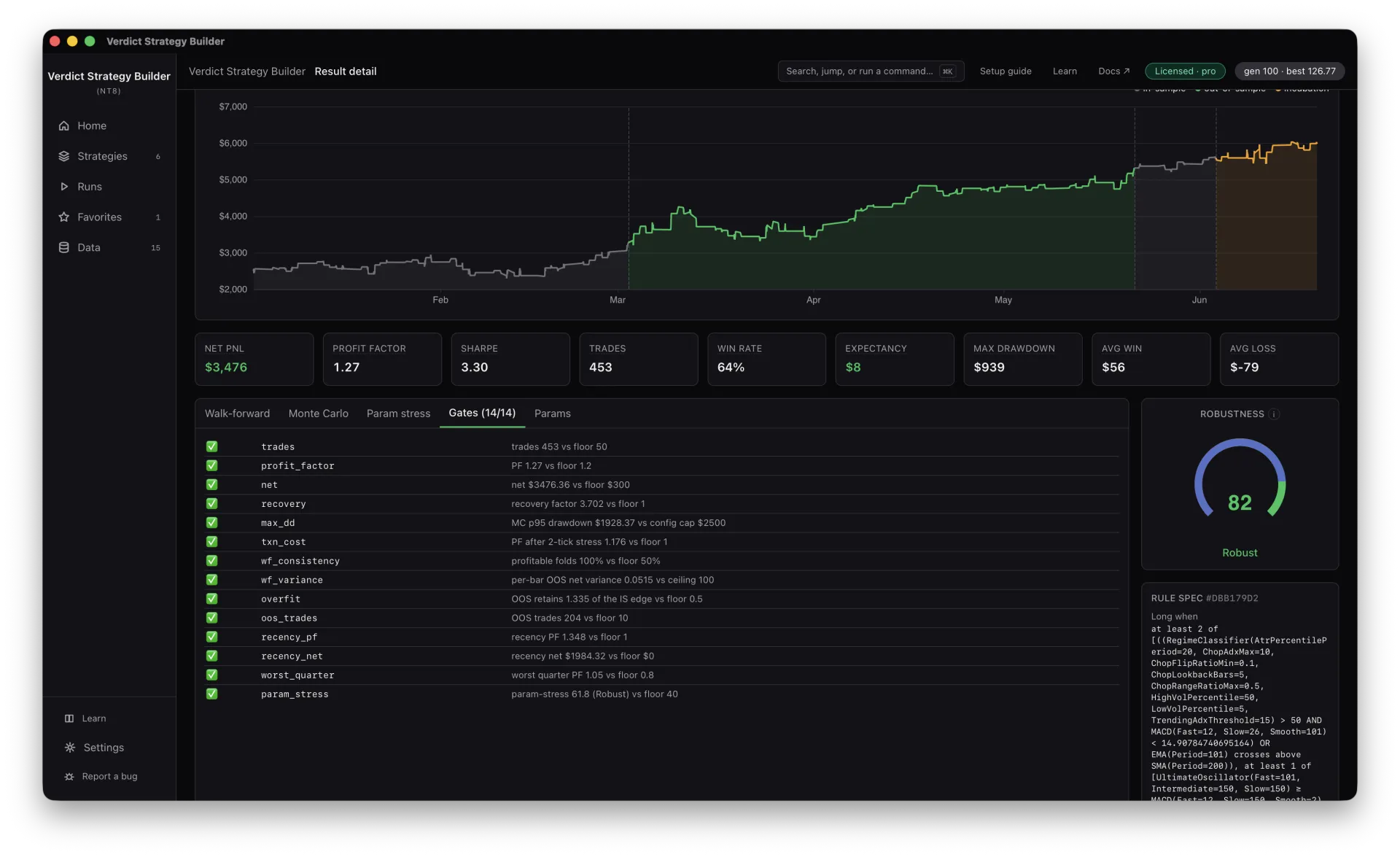

Quality gates & the verdict

Finally, a fixed battery of gates — minimum trades, profit factor floor, out-of-sample consistency, transaction-cost survival and more — must all pass. Clear them and a strategy earns its verdict; miss one and you see exactly which.

- A consistent, pre-declared bar every finalist must clear

- Pass, Marginal or Kill — with the failing gate named

- No cherry-picking: the same gates apply to every candidate

Validation, explained

What is curve-fitting (overfitting)?

It’s tuning a strategy so tightly to past data that it captures noise instead of a repeatable edge. Curve-fit strategies show beautiful backtests and then fall apart live, because the exact patterns they memorised don’t recur. Validation exists to catch them before your money does.

Why isn’t a good backtest enough?

Because with enough parameters you can make almost any backtest look great on one slice of history. The question that matters is whether performance holds on data the strategy was never fitted to — which is exactly what walk-forward, out-of-sample and Monte Carlo testing measure.

Does validation guarantee future profits?

No. Nothing can — markets change and every result carries risk. Validation improves your odds by rejecting strategies that only ever worked in-sample, so what you trade has at least survived being attacked from several directions.

Do I have to run all of this myself?

No — it’s automatic. Verdict Strategy Builder runs walk-forward, Monte Carlo, parameter-stress and the quality gates on every finalist and rolls the result into a single verdict, so rigorous validation is the default, not a chore.

Trade what survived the test

Let every candidate face walk-forward, Monte Carlo and parameter-stress before it ever reaches your charts.